What Is the Cost of Factoring?

Cost of factoring is the total expense a business pays to convert unpaid invoices into working capital, often within 24 hours, through a factoring company. It includes the factoring rate, discount fee, service fee, advance rate impact, reserve amount, and any additional charges deducted before the final payout.

Invoice factoring fees commonly range between 1.5% and 5% of the invoice value, depending on customer creditworthiness, payment terms, invoice volume, and agreement structure. Higher-risk customers, longer repayment periods, and lower transaction volume usually increase the total factoring cost.

Unlike loan interest, factoring cost comes from selling accounts receivable rather than borrowing capital. Businesses use factoring to improve cash flow, cover operating expenses, fund payroll, or manage working capital while waiting for customers to pay outstanding invoices.

What Are the Main Components of Factoring Cost?

Factoring costs include multiple charges tied to invoice funding, customer payment risk, and agreement terms.

- Discount Fees: Primary factoring charge applied to invoice value for advancing funds against accounts receivable. Factoring rates commonly range between 1% and 5% depending on payment terms, customer creditworthiness, and invoice risk.

- Service Charges: Administrative costs connected to collections, account management, invoice verification, and reporting activities. Some factoring companies include these costs inside the factoring rate, while others charge them separately.

- Reserve Deductions: Temporary portion of invoice value held until customer payment is completed successfully. Reserve amounts often range between 5% and 30% depending on advance rate structure and invoice risk level.

- Processing Costs: Wire transfers, ACH payments, invoice submissions, and same-day funding requests may create additional transaction expenses. Frequent invoice activity can increase total processing-related costs over time.

- Contract Penalties: Monthly minimum requirements, inactivity charges, and early termination fees may apply under long-term factoring agreements. Contract-based expenses vary depending on provider terms and funding structure.

How Do You Calculate Factoring Fees?

Factoring fees are calculated using invoice value, factoring rate, advance percentage, reserve amount, payment terms, customer creditworthiness, and additional agreement-based charges.

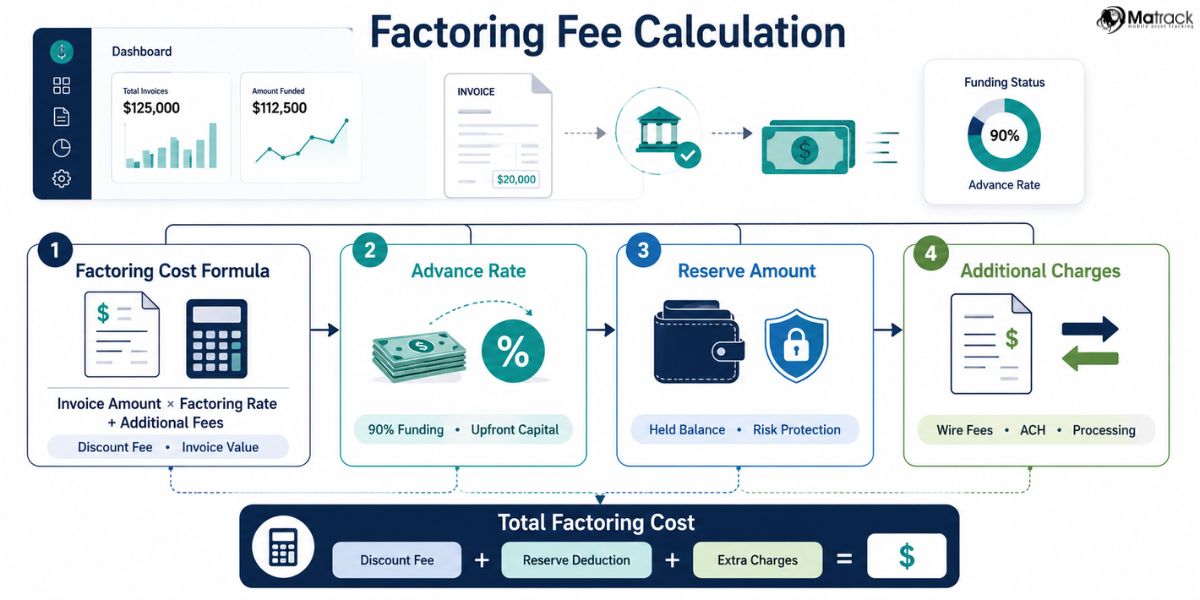

Factoring Cost Formula

Most factoring companies calculate invoice factoring cost by applying the discount fee to the invoice amount. Processing costs, service charges, wire fees, or contract-related expenses are then added to find the total factoring cost.

Invoice Amount × Factoring Rate + Additional Fees = Total Factoring Cost

A $20,000 invoice with a 3% factoring rate creates a $600 discount fee. Extra charges such as processing or transfer fees increase the final cost deducted from invoice proceeds.

Advance Rate

Advance rate determines how much upfront working capital a business receives before customer payment is collected. Factoring providers calculate advance percentages using invoice quality, payment history, industry risk, transaction volume, and customer credit profile.

A 90% advance rate on a $20,000 invoice provides $18,000 in immediate funding. The remaining invoice value stays temporarily with the factoring company as the reserve amount.

Reserve Amount

Reserve amount is the portion of invoice value held against disputes, deductions, late payments, or non-payment risk. Factoring companies release reserve balances after customer payment clears and all factoring costs are deducted.

Final payout depends on total factoring fees, payment timing, reserve release terms, and additional charges listed in the factoring agreement. Delayed customer payments can reduce the remaining balance under tiered or variable pricing structures.

Additional Charges

Additional factoring costs may include invoice processing fees, ACH charges, wire transfer fees, same-day funding costs, credit check fees, monthly minimum charges, and contract termination penalties. Small recurring expenses can increase the effective annual factoring cost over multiple invoice cycles.

Businesses should review all fee disclosures before signing a factoring contract tied to accounts receivable financing. Written pricing details help compare providers beyond the advertised factoring rate.

What Is the Effective Annual Cost of Factoring?

Effective annual factoring cost is the yearly impact of using invoice factoring repeatedly across multiple funding cycles. Small monthly factoring charges can become expensive when discount fees, service charges, processing costs, and reserve deductions continue throughout the year.

Factoring agreements may apply fees weekly, monthly, or based on invoice age depending on the pricing structure. Longer customer payment terms, delayed collections, tiered rates, and variable pricing usually increase total accounts receivable financing costs over time.

Annualized factoring cost helps businesses compare invoice factoring with loans, credit lines, invoice financing, or other working capital solutions. Cost comparison also shows whether improved cash flow justifies the reduction in profit margin after factoring fees are deducted.

What Factors Affect Invoice Factoring Rates?

Invoice factoring rates depend on how much risk, time, and administrative work the factoring company takes on.

- Customer Credit: Customer creditworthiness directly affects the factoring rate because the customer is responsible for paying the invoice. Reliable payment history, strong credit profile, and fewer disputes usually reduce collection risk.

- Payment Terms: Payment terms influence cost because longer invoice cycles keep the factor’s funds tied up for more time. A 30-day invoice usually costs less than a 60-day or 90-day invoice.

- Invoice Volume: Invoice volume affects pricing because consistent receivables create predictable funding activity for the factoring company. Higher transaction volume may help businesses negotiate lower discount fees or better advance terms.

- Industry Risk: Industry risk matters when payment delays, customer disputes, or collection issues are common in a business sector. Factoring companies may charge higher rates for industries with unpredictable accounts receivable cycles.

- Invoice Quality: Invoice quality improves pricing when invoices are accurate, verified, undisputed, and tied to completed work. Missing documents, billing errors, or disputed amounts can increase factoring costs.

- Factoring Type: Factoring type changes cost because recourse and non-recourse agreements carry different risk levels. Recourse factoring usually costs less, while non-recourse factoring often costs more because the factor accepts greater payment risk.

How Do Recourse and Non-Recourse Factoring Affect Cost?

Recourse and non-recourse factoring affect cost by changing who carries the financial risk when a customer fails to pay an invoice.

| Factor | Recourse Factoring | Non-Recourse Factoring |

| Payment Risk | Business remains responsible if the customer does not pay. | Factoring companies accept specific non-payment risks defined in the contract. |

| Typical Cost | Usually lower because the factor carries less risk. | Usually higher because the factor accepts more credit exposure. |

| Customer Credit Role | Customer credit still matters, but risk stays partly with the business. | Customer credit is more important because the factor may absorb payment failure. |

| Chargebacks | Factor may charge the invoice back to the business if payment fails. | Chargebacks may be limited, depending on covered risk conditions. |

| Best Fit | Works well for businesses with reliable customers and predictable payments. | Works well when customer credit risk is higher or protection is more important. |

| Contract Review | Check repayment obligations, reserve terms, and chargeback rules. | Check exclusions, dispute limits, insolvency coverage, and non-payment conditions. |

What Hidden Fees Should You Watch For?

Hidden fees can raise invoice financing costs beyond the advertised factoring rate.

- Setup Fees: Account opening or onboarding charges can appear before the first invoice is funded. These costs matter most when a business only plans to factor invoices occasionally.

- Processing Fees: Invoice review, document handling, payment posting, or account updates can create recurring expenses. High transaction volume makes these small charges more noticeable over time.

- Wire Fees: Same-day transfers usually cost more than standard ACH deposits. Businesses using urgent funding often should compare speed against transfer cost.

- Credit Checks: Customer credit reviews can add extra charges during invoice approval. Riskier account debtors often require deeper verification before funding is released.

- Monthly Minimums: Minimum volume requirements can trigger charges if invoice activity falls below the contract threshold. Seasonal businesses should check this term before signing.

- Inactivity Charges: Unused accounts can still create costs during slow sales periods. Irregular cash flow businesses should avoid agreements that punish low funding activity.

- Late Payment Costs: Delayed customer payments can increase fees under tiered or variable pricing. Longer collection periods reduce the final amount released from the reserve.

- Termination Penalties: Early cancellation can become expensive when contracts include long terms or strict exit rules. Review notice periods, renewal dates, and cancellation language closely.

- Renewal Terms: Automatic renewal clauses can extend the agreement if cancellation deadlines are missed. Clear contract tracking helps prevent unwanted long-term costs.

How Can You Reduce Factoring Fees?

Businesses can reduce factoring fees by lowering payment risk, improving invoice quality, and negotiating stronger agreement terms.

Improve Customer Payments

Reliable customers with consistent payment history usually qualify for lower factoring rates, since payment risk is lower. Faster invoice payments also reduce charges linked to long collection periods and unpaid accounts receivable.

Shorten Payment Terms

Shorter payment terms reduce the time between invoice funding and customer repayment. Thirty-day receivables usually cost less to factor than longer payment cycles because the factoring company recovers funds sooner.

Increase Invoice Volume

Steady invoice volume can improve negotiating power during pricing discussions. Higher transaction activity gives the factoring company more predictable funding opportunities, which can support lower discount fees.

Compare Providers

Factoring companies use different pricing models, reserve terms, service charges, and contract rules. Comparing full fee schedules helps businesses identify the true financing cost instead of relying only on the advertised factoring rate.

Avoid Extra Charges

Wire transfers, same-day funding requests, unnecessary account services, and avoidable processing fees can increase total expenses. Reviewing fee disclosures carefully helps prevent small charges from becoming recurring factoring costs.

Review Contract Terms

Long-term agreements may include renewal clauses, inactivity penalties, monthly minimums, or early termination charges. Flexible contract terms help reduce long-term financial risk tied to invoice factoring.

Choose Suitable Factoring Type

Recourse factoring usually costs less because the business keeps more payment responsibility. Non-recourse factoring can cost more because the factoring company accepts greater risk for customer non-payment.

Final Thoughts

Cost of factoring includes discount fees, service charges, reserve deductions, processing costs, contract penalties, and other expenses tied to accounts receivable funding. Invoice value, customer creditworthiness, payment terms, industry risk, advance rate, and factoring structure all influence the final financing cost.

Factoring fees are calculated using the invoice amount, factoring rate, additional charges, reserve terms, and customer payment timing. Businesses comparing factoring providers should review full fee schedules carefully instead of focusing only on the advertised discount rate.

Lower factoring costs usually come from reliable customer payments, shorter invoice cycles, stronger receivables, higher invoice volume, and flexible agreement terms. Proper cost analysis helps businesses decide whether invoice factoring provides enough working capital value to justify the total financing expense.